All Categories

Featured

Table of Contents

- – Why do I need Level Term Life Insurance Policy?

- – Is there a budget-friendly Level Term Life Ins...

- – What is the best Best Value Level Term Life I...

- – What is a simple explanation of Level Term Li...

- – What does a basic What Is Level Term Life In...

- – Who offers flexible Level Term Life Insuranc...

Term life insurance coverage is a kind of plan that lasts a particular size of time, called the term. You select the size of the plan term when you initially take out your life insurance.

Choose your term and your amount of cover. Select the policy that's right for you., you understand your costs will certainly remain the very same throughout the term of the plan.

Why do I need Level Term Life Insurance Policy?

(Nonetheless, you do not get any kind of refund) 97% of term life insurance policy cases are paid by the insurer - SourceLife insurance covers most conditions of fatality, yet there will certainly be some exemptions in the terms of the plan. Exemptions might consist of: Genetic or pre-existing problems that you fell short to reveal at the beginning of the policyAlcohol or medication abuseDeath while dedicating a crimeAccidents while participating in unsafe sportsSuicide (some policies leave out death by self-destruction for the initial year of the policy) You can add vital disease cover to your level term life insurance for an additional cost.Critical illness cover pays a portion of your cover amount if you are diagnosed with a serious disease such as cancer, cardiac arrest or stroke.

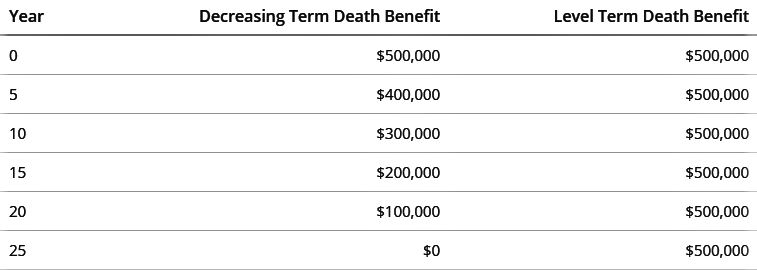

Hereafter, the plan ends and the enduring companion is no much longer covered. Individuals typically obtain joint plans if they have impressive economic commitments like a home mortgage, or if they have kids. Joint policies are normally extra inexpensive than single life insurance policy plans. Various other kinds of term life insurance policy policy are:Decreasing term life insurance policy - The quantity of cover decreases over the size of the plan.

This safeguards the buying power of your cover amount against inflationLife cover is a wonderful thing to have due to the fact that it gives monetary defense for your dependents if the worst occurs and you die. Your loved ones can also use your life insurance policy payment to spend for your funeral. Whatever they choose to do, it's fantastic comfort for you.

However, level term cover is great for satisfying day-to-day living costs such as home costs. You can likewise use your life insurance policy benefit to cover your interest-only home mortgage, repayment home mortgage, school fees or any other financial obligations or recurring settlements. On the various other hand, there are some downsides to level cover, contrasted to other sorts of life policy.

Is there a budget-friendly Level Term Life Insurance option?

The word "degree" in the expression "degree term insurance" suggests that this kind of insurance policy has a set premium and face quantity (death advantage) throughout the life of the policy. Just placed, when people discuss term life insurance coverage, they normally refer to level term life insurance policy. For most of individuals, it is the most basic and most cost effective option of all life insurance policy types.

The word "term" here refers to a given variety of years during which the level term life insurance policy remains active. Degree term life insurance policy is just one of one of the most popular life insurance policy policies that life insurance policy providers offer to their clients as a result of its simplicity and affordability. It is also simple to compare level term life insurance policy quotes and get the ideal premiums.

The system is as complies with: First of all, pick a plan, death advantage amount and plan period (or term size). Choose to pay on either a regular monthly or yearly basis. If your premature demise takes place within the life of the plan, your life insurer will pay a swelling amount of survivor benefit to your predetermined beneficiaries.

What is the best Best Value Level Term Life Insurance option?

Your level term life insurance plan expires as soon as you come to the end of your policy's term. Option B: Buy a brand-new degree term life insurance plan.

Your current web browser could restrict that experience. You may be using an old web browser that's unsupported, or settings within your browser that are not suitable with our site.

What is a simple explanation of Level Term Life Insurance Companies?

Already using an upgraded internet browser and still having problem? Your present web browser: Spotting ...

If the policy expires before runs out prior to or you live beyond the past term, there is no payout. You may be able to restore a term policy at expiration, but the costs will certainly be recalculated based on your age at the time of revival.

Whole Life Insurance Rates 30 $282 $247 40 $382 $352 50 $571 $498 60 $887 $782 Source: Quotacy. Quotes are for a $500,000 irreversible life insurance plan, for men and ladies in exceptional health and wellness.

What does a basic What Is Level Term Life Insurance? plan include?

That lowers the total risk to the insurance firm contrasted to a long-term life plan. The reduced threat is one factor that allows insurance companies to charge reduced premiums. Rates of interest, the financials of the insurance business, and state policies can likewise influence costs. As a whole, companies frequently offer better prices at the "breakpoint" protection levels of $100,000, $250,000, $500,000, and $1,000,000.

Inspect our referrals for the ideal term life insurance plans when you are all set to purchase. Thirty-year-old George desires to shield his household in the unlikely event of his sudden death. He buys a 10-year, $500,000 term life insurance policy with a premium of $50 monthly. If George passes away within the 10-year term, the policy will certainly pay George's beneficiary $500,000.

If he lives and renews the plan after ten years, the costs will certainly be higher than his first plan due to the fact that they will be based upon his current age of 40 rather than 30. Level death benefit term life insurance. If George is detected with an incurable illness during the very first plan term, he possibly will not be qualified to restore the plan when it expires

There are a number of kinds of term life insurance policy. The most effective option will depend upon your private situations. Usually, a lot of firms offer terms ranging from 10 to three decades, although a couple of deal 35- and 40-year terms. Level-premium insurance has a fixed month-to-month settlement for the life of the plan. Most term life insurance has a level premium, and it's the type we've been describing in the majority of this write-up.

Who offers flexible Level Term Life Insurance Quotes plans?

Therefore, the costs can end up being much too costly as the policyholder ages. Yet they might be a great option for someone that needs short-lived insurance. These plans have a fatality advantage that declines yearly according to an established timetable. The insurance holder pays a fixed, level costs throughout of the policy.

{kind=link}

Table of Contents

- – Why do I need Level Term Life Insurance Policy?

- – Is there a budget-friendly Level Term Life Ins...

- – What is the best Best Value Level Term Life I...

- – What is a simple explanation of Level Term Li...

- – What does a basic What Is Level Term Life In...

- – Who offers flexible Level Term Life Insuranc...

Latest Posts

What is Level Term Vs Decreasing Term Life Insurance? Key Points to Consider?

What is the Appeal of 20-year Level Term Life Insurance?

What is Term Life Insurance With Level Premiums? Learn the Basics?

More

Latest Posts

What is Level Term Vs Decreasing Term Life Insurance? Key Points to Consider?

What is the Appeal of 20-year Level Term Life Insurance?

What is Term Life Insurance With Level Premiums? Learn the Basics?