All Categories

Featured

Table of Contents

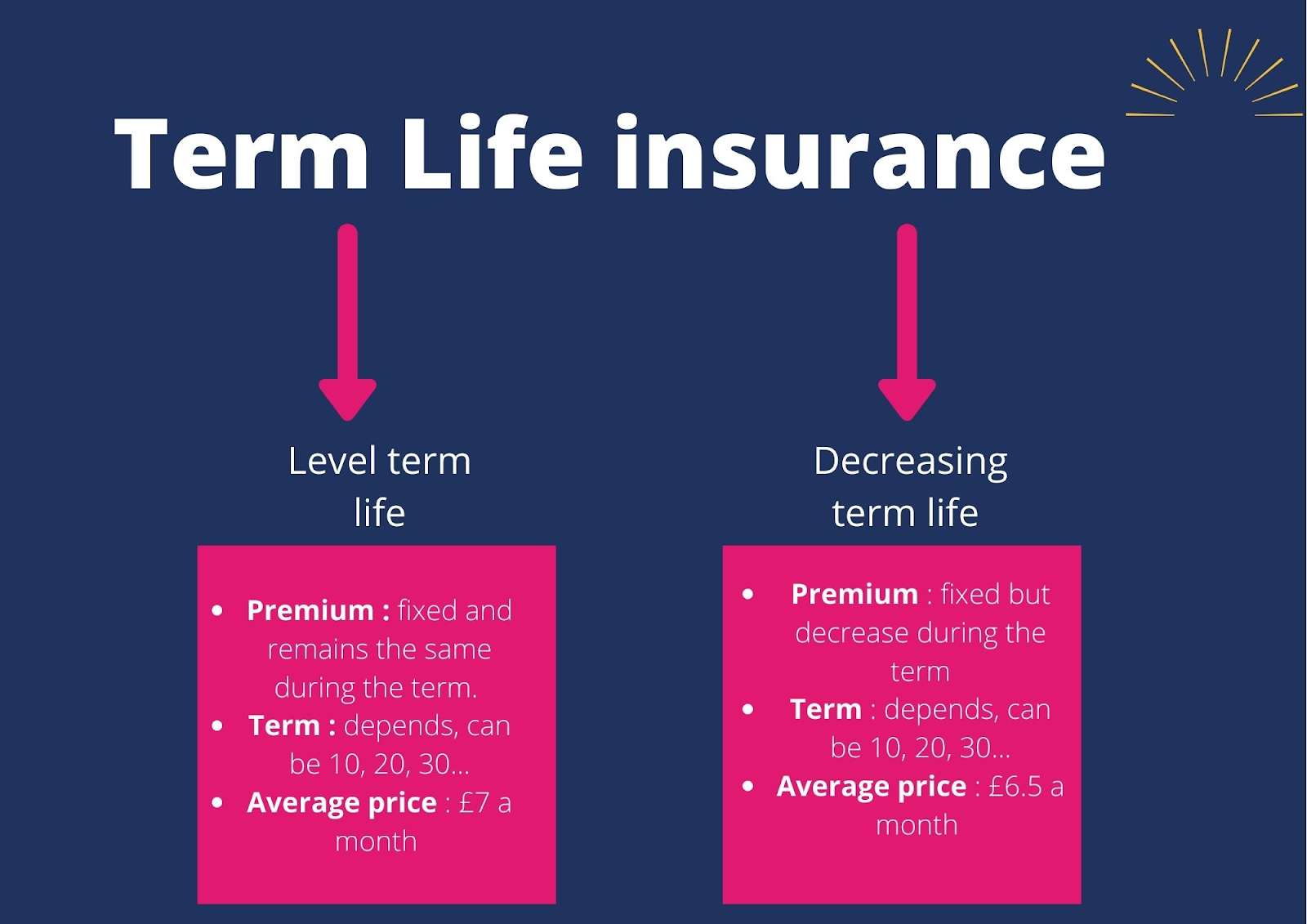

Term plans are also usually level-premium, however the overage amount will continue to be the same and not grow. The most typical terms are 10, 15, 20, and three decades, based upon the needs of the insurance holder. Level-premium insurance is a kind of life insurance coverage in which premiums stay the exact same rate throughout the term, while the amount of insurance coverage used boosts.

For a term plan, this indicates for the size of the term (e.g. 20 or thirty years); and for an irreversible policy, until the insured passes away. Level-premium policies will normally set you back even more up-front than annually-renewing life insurance policy plans with regards to only one year each time. Over the long run, level-premium settlements are frequently extra cost-effective.

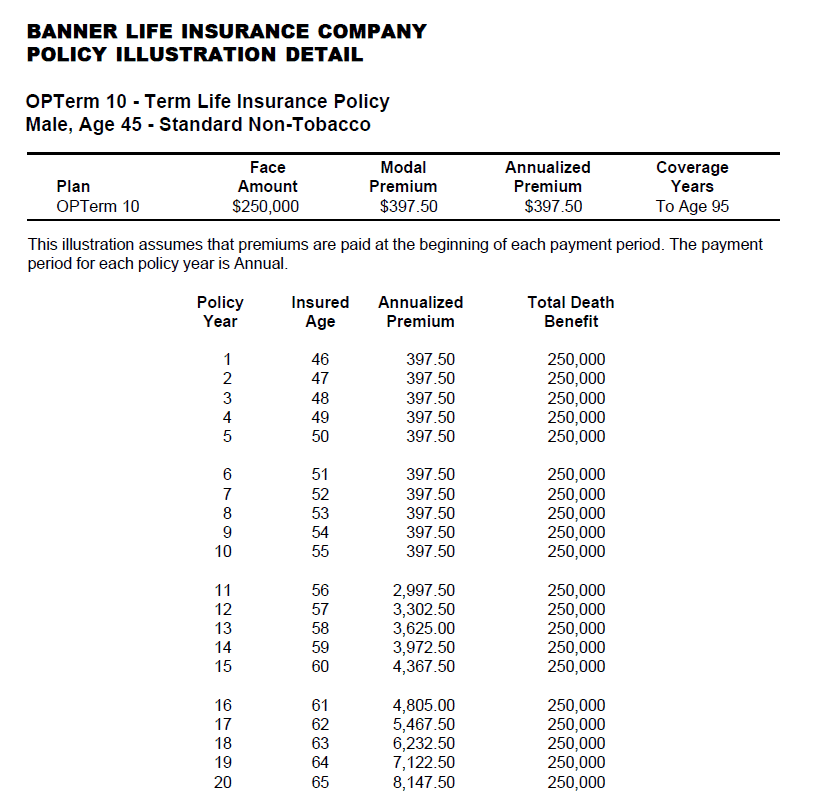

They each seek a 30-year term with $1 million in protection. Jen purchases an assured level-premium policy at around $42 each month, with a 30-year perspective, for an overall of $500 each year. Yet Beth figures she might just require a prepare for three-to-five years or up until full settlement of her existing financial debts.

In year 1, she pays $240 per year, 1 and about $500 by year 5. In years two through five, Jen proceeds to pay $500 per month, and Beth has actually paid approximately simply $357 each year for the exact same $1 countless coverage. If Beth no more requires life insurance policy at year five, she will have conserved a great deal of money about what Jen paid.

What is Life Insurance Level Term? Key Considerations?

Each year as Beth grows older, she faces ever-higher annual premiums. Jen will certainly proceed to pay $500 per year. Life insurers have the ability to offer level-premium plans by essentially "over-charging" for the earlier years of the policy, gathering even more than what is needed actuarially to cover the danger of the insured passing away throughout that very early duration.

Permanent life insurance coverage establishes money value that can be borrowed. Policy fundings build up passion and unpaid policy loans and interest will lower the fatality advantage and cash money value of the policy. The quantity of cash money value offered will usually depend on the kind of permanent plan bought, the amount of protection bought, the length of time the plan has actually been in pressure and any outstanding plan loans.

A complete statement of insurance coverage is found just in the plan. Insurance coverage policies and/or linked bikers and functions might not be available in all states, and plan terms and problems might vary by state.

Level term life insurance is the most simple way to get life cover. In this post, we'll describe what it is, how it works and why degree term may be appropriate for you.

Is Direct Term Life Insurance Meaning a Good Option for You?

Term life insurance policy is a kind of policy that lasts a certain length of time, called the term. You choose the size of the plan term when you initially take out your life insurance coverage.

Select your term and your quantity of cover. You might have to address some concerns about your case history. Select the plan that's right for you - Life insurance level term. Now, all you have to do is pay your premiums. As it's level term, you understand your costs will stay the same throughout the regard to the policy.

(Nonetheless, you don't receive any kind of cash back) 97% of term life insurance policy cases are paid by the insurance provider - ResourceLife insurance coverage covers most scenarios of death, however there will certainly be some exemptions in the terms of the plan. Exclusions may include: Genetic or pre-existing problems that you failed to disclose at the beginning of the policyAlcohol or drug abuseDeath while devoting a crimeAccidents while taking part in harmful sportsSuicide (some policies leave out fatality by self-destruction for the very first year of the policy) You can include critical health problem cover to your degree term life insurance policy for an added expense.Critical ailment cover pays a portion of your cover amount if you are identified with a serious ailment such as cancer cells, heart attack or stroke.

After this, the plan ends and the making it through companion is no much longer covered. Joint plans are typically more affordable than single life insurance coverage policies.

What is What Is Direct Term Life Insurance? An Essential Overview?

This safeguards the acquiring power of your cover quantity versus inflationLife cover is an excellent point to have due to the fact that it offers monetary protection for your dependents if the worst occurs and you die. Your liked ones can likewise utilize your life insurance policy payout to pay for your funeral. Whatever they pick to do, it's excellent comfort for you.

Degree term cover is great for satisfying daily living expenditures such as house bills. You can likewise utilize your life insurance benefit to cover your interest-only mortgage, payment home loan, college costs or any other financial debts or ongoing payments. On the other hand, there are some drawbacks to level cover, compared to various other kinds of life plan.

Term life insurance policy is a budget friendly and simple choice for lots of people. You pay costs monthly and the coverage lasts for the term length, which can be 10, 15, 20, 25 or three decades. Term life insurance with accidental death benefit. What occurs to your premium as you age depends on the type of term life insurance policy coverage you purchase.

What is Decreasing Term Life Insurance? Comprehensive Guide

As long as you continue to pay your insurance policy premiums each month, you'll pay the same rate throughout the whole term length which, for numerous term policies, is commonly 10, 15, 20, 25 or thirty years. When the term finishes, you can either pick to end your life insurance protection or renew your life insurance coverage plan, typically at a greater rate.

As an example, a 35-year-old female in exceptional wellness can acquire a 30-year, $500,000 Place Term plan, released by MassMutual beginning at $29.15 each month. Over the following three decades, while the policy is in location, the cost of the coverage will certainly not transform over the term duration - What is a level term life insurance policy. Let's admit it, a lot of us don't such as for our bills to expand with time

Your level term price is determined by a number of factors, most of which are connected to your age and health and wellness. Various other aspects include your specific term plan, insurance supplier, benefit quantity or payout. Throughout the life insurance policy application procedure, you'll answer questions regarding your health background, consisting of any type of pre-existing conditions like a vital ailment.

{kind=link}

Latest Posts

Instant Issue Term Life Insurance

Final Benefits Insurance

No Exam Instant Life Insurance